Introduction to Startup Valuation

A deep dive into how Venture Capitalists assess and estimate the value of startups. The VC Method.

Startup valuation is only an estimation; there is no exact science.

Before we dive in, it's worth noting that there are several ways to put a price tag on a startup, and these methods often serve the purpose of supporting the preferences of the folks doing the evaluation.

In this post, I'll be tackling a variety of interesting topics, from the different phases a startup goes through to some important factors in sizing up a startup, the external forces that can mess with its value, and the favourite method that most Venture Capitalists lean on when they're valuing startups.

Each stage has specific characteristics that fit better with one type of investor or another, depending on their risk aversion.

Different stages can be identified in a startup, but I will give my 2 cents about the initial ones: Pre-seed, Seed, Series A, and Expansion (Series A onwards).

The pre-seed stage is the most embryonic phase of a startup, where the founding team comes together, the business idea is developed, and a prototype is made. The valuation of startups at this stage is a complex process linked to the lack of information about the company (practically no revenue, users, etc.). This is why investors usually base their investment decision on the growth potential of the company, mainly determined by the market and the quality of the founding team. Another important factor to consider is risk. Companies at this stage have a high level of risk, as there is usually great uncertainty about market demand.

Seed Stage: The startup begins to have a clearer business model and target customers who are genuinely interested in the solution. During this stage, apart from the team and market, investors are usually interested in the viability of the business model.

In Series A, which would be the growth stage, the startup begins to experience greater growth and can expand into new markets. At this stage, investors focus on the path to profitability.

Finally, from this stage, there would be the Expansion and Maturity Stage, Series B, C, D, etc., where the startup focuses on geographical expansion, market consolidation, and eventually becomes profitable.

Regardless of the stage, there are several key factors that investors must carefully consider to make an investment decision.

Founding Team: The experience and skills of the founding team are fundamental. Typically, a team with relevant experience in the sector, complementary skills, and above all, the ability to adapt to change, has higher chances to success.

Market: The size of the potential market for the startup is a very important factor. It is necessary to understand if the startup has a large enough market for venture capitalists to be interested, if there is demand for the product or service, and the future market share the company could have. That said, there are many good businesses offering a solution in small markets that are very respectable and profitable. They may have difficulty raising funds from venture capital investors, but it does not mean they are bad businesses.

Competition: It must be understood if the startup has a competitive advantage and if it can compete in the market effectively.

Business Model: The way the startup generates revenue and its scalability are also key elements. They must have a sustainable business model and interesting long-term growth potential. The more efficient the entrepreneur is with capital, the greater the multiple will be for the investor at exit.

There are different external factors that influence valuations.

In my opinion, one of the most relevant factors influencing the valuation of a startup is the supply and demand between investors and entrepreneurs. If there are many investors competing to invest in a startup, it can generate a higher valuation, as investors are willing to pay more to secure participation in the company. Conversely, where the number of startups is much larger than the number of investors willing to invest, can negatively affect valuation. In fact, I have experienced several cases where the valuation has drastically changed in the same round as entrepreneurs talked to investors.

Apart from that, emerging industries (like AI), the macroeconomic situation, and entrepreneur's need to capital, are factors that have a direct effect in valuations.

The VC Method - One of the most commonly used methods by venture capital investors

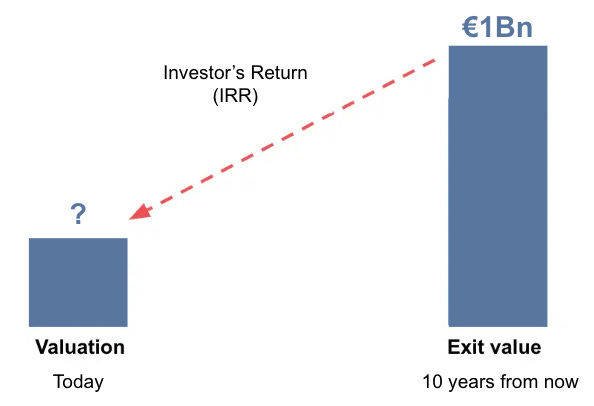

When an investor analyzes a startup, regardless of the stage it's in, what they seek is to predict the outcome of the company, that is, the valuation at the time of exit. Once they have estimated the size of the exit, the investor must determine how much ownership they should have at the time of exit to achieve their target return. To get this, one must consider the amount of money invested in the company from the beginning, the valuation at the time of investment, and the dilution that has occurred in subsequent rounds.

Based on these assumptions, investors decide how much ownership in the company they need so that when the startup exits, they achieve their target return.

VC investment funds work under the J curve and want to invest in startups that have the potential to generate a return of the total fund. Therefore, investors make assumptions about the company's growth in the coming years and estimate a startup's exit value to see if they can achieve the multiple or return they seek.

This method dissects the valuation problem into 4 fundamental questions:

What valuation will the company achieve at a given time?

What return is intended to be achieved?

How much equity should be held at the time of the sale?

What dilution will there be or what disbursements will have to be made over time to maintain this level of equity?

Example of the VC Method

This would be in an ideal world, but in reality, early-stage investors dilute over time as entrepreneurs raise more capital before the exit.

The example we just saw assumes the valuation at the time of the exit (€200m). An easy way to project this, despite being speculative, is based on multiples in comparable transactions.

Comparable Transactions

Comparables are based on precedents and measure how other companies are valued in the market based on some criteria (for example, revenue multiples) that can be applied to the company as a proxy for the current value.

It is important to select comparables from companies that are as similar as possible to yours (same market, geography, business model, etc.).

Despite not being an exact science, it combines multiple factors based on your knowledge and market benchmarks, allowing you to make calibrated estimates.

🤔Carta, Pitchbook, Crunchbase or CBInsights are good sources of knowledge and databases to find benchmarks.

Great job